Forward Implied Volatility Term Structure

This is an application that displays the forward implied at-the-money volatility term structure for Bitcoin options in real time.

Methodology

“At-the-money” in this case is defined as the option with the strike price nearest to the underlying forward price. As the forward price rarely falls precisely on an exact strike, a linear interpolation is made between the volatilities of the two options with the nearest strikes (above and below) the forward. For option tenors without a corresponding listed forward, a similiar linear interpolation is made between the prices of the forwards nearest to the option tenor.

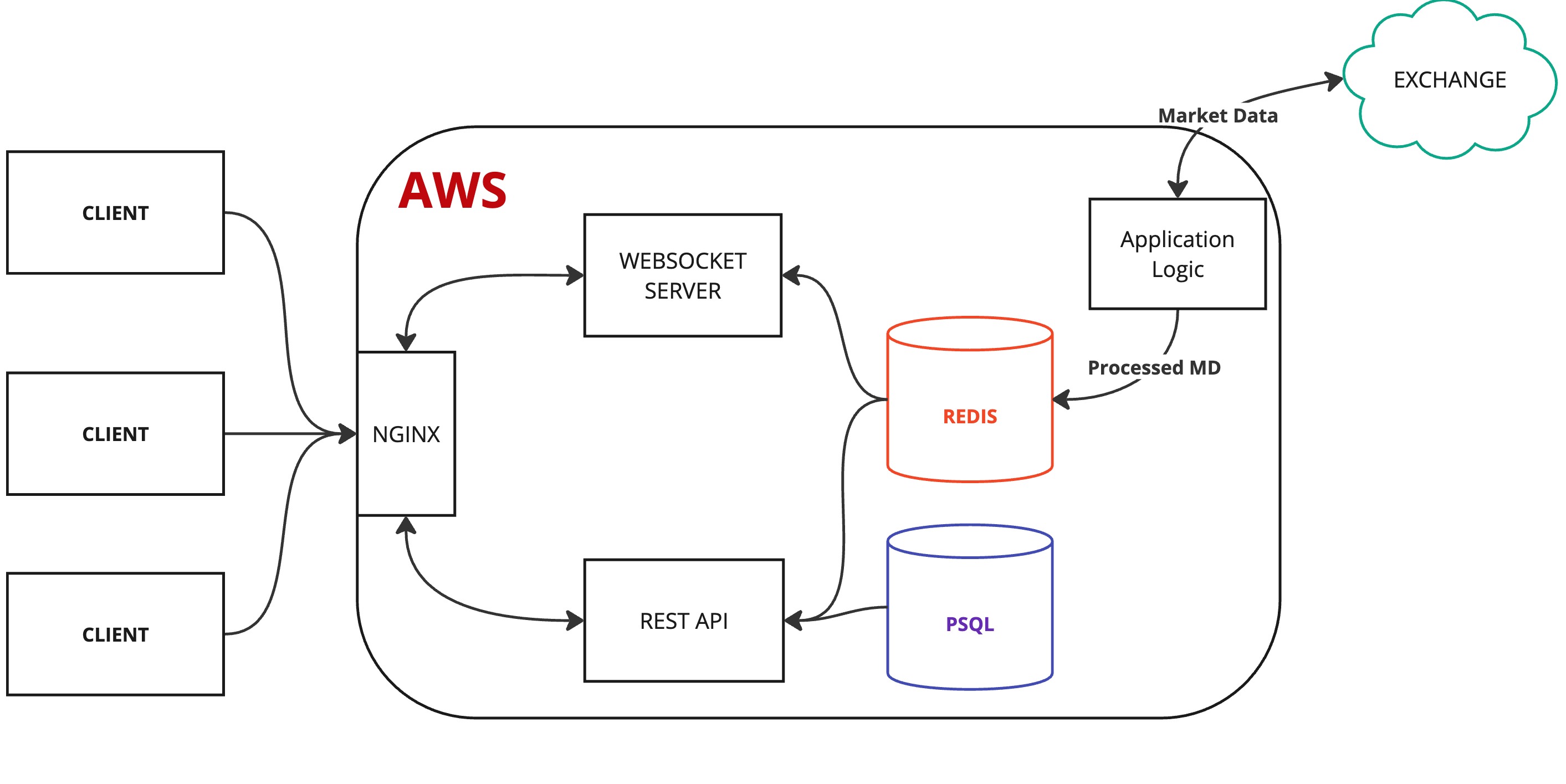

Architecture

A diagram of the application architecture is pictured below. The primary application receives market data via websocket from a leading derivatives exhange. That MD is procecessed and published to Redis using Redis’s publish/subscibe paradigm.

Clients connect to the server and Nginx routes traffic to a websocket server and a REST API (built with FastAPI) as appropriate. The REST API is responsible for sending back static configuration data contained in both Redis and a PostgreSQL database. The websocket server subscribes to the processed market data being published to Redis and handles incoming client connections, broadcasting the processed MD to client subscribers.

Application Architecture

Visualization:

The visualization is a Typescript/React application leveraging WebSockets and Recharts